FHFA, other agencies announce extension of COVID-related policies

On Aug. 26, the Federal Housing Finance Agency (FHFA) announced an extension of its policies providing for Fannie Mae and Freddie Mac (the GSEs) to continue to purchase loans that entered a COVID-related forbearance prior to purchase. The GSEs’ policies were set to expire Aug. 31, but the announcement extends the policies to Sept. 30.

The policy extensions also include processing flexibilities allowed as a result of the pandemic, such as alternative methods for documenting income and verifying employment. You can view the FHFA announcement at their website.

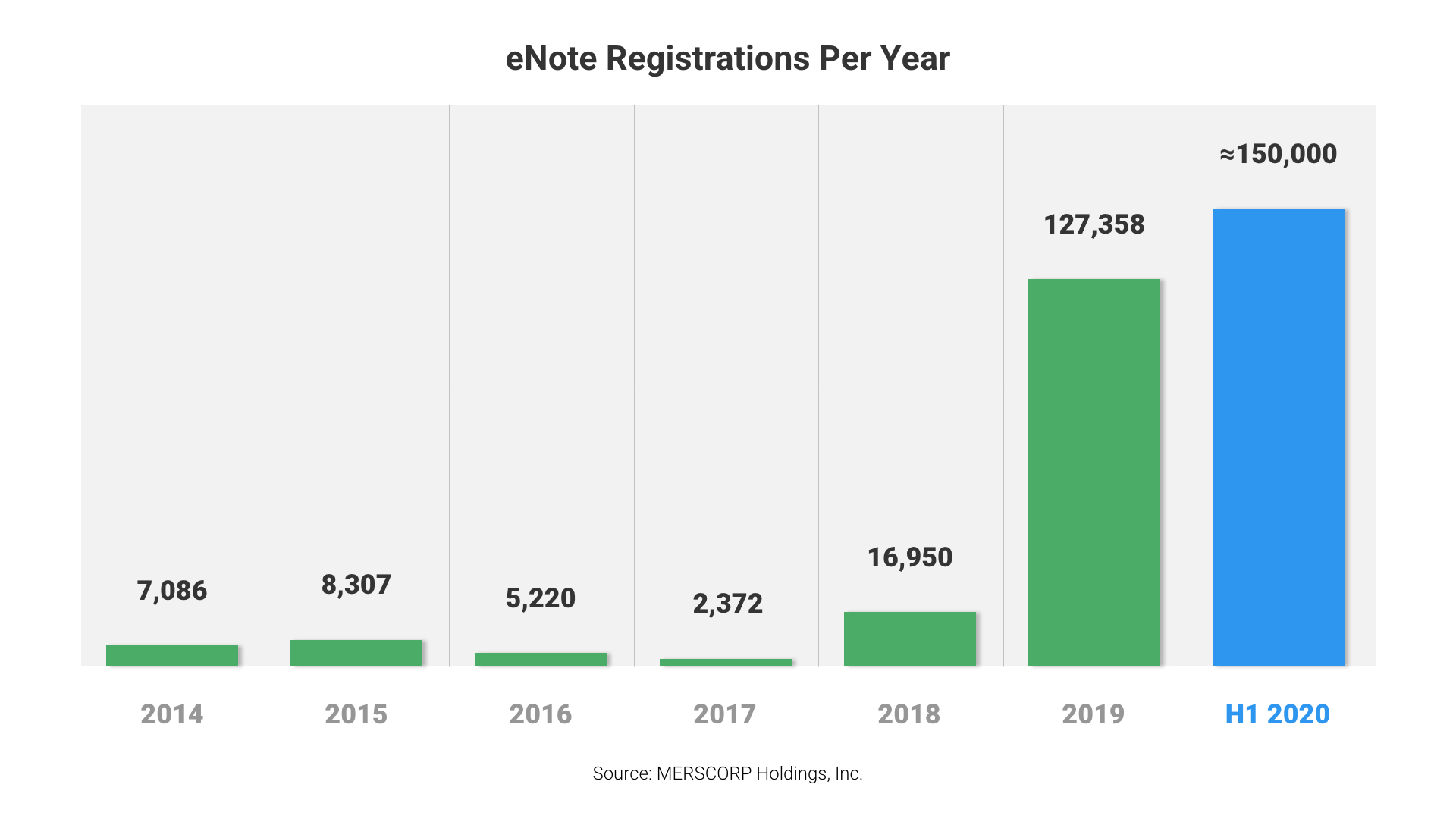

RON: The last mile in the eClosing marathon

Additionally, on Aug. 27, HUD and the GSEs announced an extension of their moratoriums on foreclosures until Dec. 31. These were previously set to also expire on Aug. 31. The extension of the GSE moratorium will “protect more than 28 million homeowners with an Enterprise-backed mortgage,” said FHFA Director Mark Calabria. The Department of Veterans Affairs announced a similar extension on Aug. 24.

In addition to the FHFA extension of processing flexibilities related to COVID, the USDA also recently announced an extension of “Temporary Exceptions in relation to COVID-19 pandemic” that include exceptions for appraisal and inspection requirements and verifications. The USDA also announced an extension of its moratorium on foreclosures similar to that of HUD and the GSEs. You can find coronavirus-related information on the USDA's website.

Related Content:

.jpg)