The Consumer Financial Protection Bureau (“CFPB”) is required to calculate annually the dollar amounts for several provisions in Regulation Z, which implements the Truth in Lending Act (“TILA”). The CFPB has issued a final rule revising the dollar amount thresholds under the Home Ownership and Equity Protection Act (“HOEPA”) and the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”). The adjustments are based on the annual percentage change in the Consumer Price Index (“CPI-U”) as of June 1, 2024.

The threshold adjustments will be effective on January 1, 2025.

HOEPA Points and Fees Thresholds

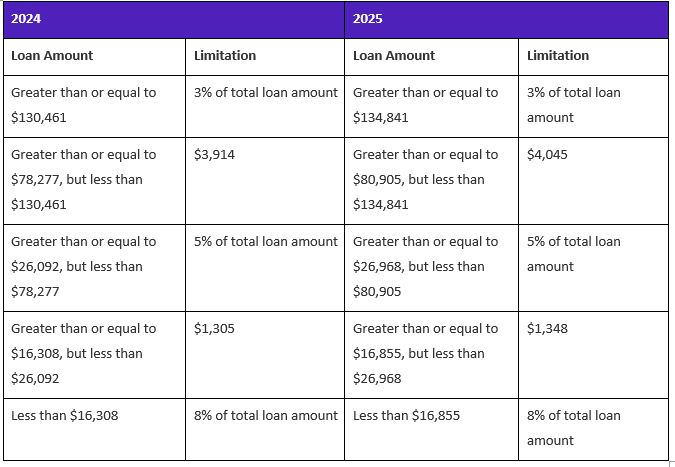

For HOEPA loans, a fee-based trigger is used to determine if a loan is subject to the “points and fees coverage test” under 12 C.F.R. § 1026.32, referred to as “Section 32” by the industry. The adjusted “points and fees” dollar trigger for high-cost mortgages will increase from $1,305 for 2024 to $1,348 for 2025. Additionally, the total loan amount threshold will increase from $ 26,092 for 2024 to $26,968 for 2025. If the total loan amount for a transaction is $26,968 or more, and the point and fees payable by the consumer at or before loan closing exceeds 5 percent of the total loan amount, the transaction is a high-cost mortgage. If the total loan amount is less than the threshold of $26,968, and the points and fees payable by the consumer at or before loan closing exceeds the lesser of the adjusted point and fees threshold of $1,348, or 8 percent of the total loan amount, the transaction is a high-cost mortgage.

In addition to the Federal Section 32 test, this adjustment applies to the following state high-cost tests: Colorado, Illinois, Maryland, Massachusetts, Oklahoma, Pennsylvania, Texas, and Utah. For more information, please click here.

To view DocMagic’s memorandum regarding HOEPA determination, please see Section 32 High-Cost Calculation.

Qualified Mortgage Points and Fees Thresholds

For all categories of qualified mortgages ("QM"), points and fees have the same meaning as "points and fees" under Section 32, but unlike Section 32, the following thresholds apply, as specified in Regulation Z (12 CFR § 1026.43(e)(3)(i)).

Qualified Mortgage Price-Based Limit Categories

For qualified mortgages (“QM”) under the general loan definition in 12 § C.F.R. 1026.43(e)(2), the thresholds for the spread between the annual percentage rate and the average prime offer rate (price-based limit) have been increased for 2025. The top loan amount category for a first-lien loan secured by a non-manufactured home will increase from $130,461 to $134,841 using a 2.25% threshold.